It goes without saying that bringing 5G to the world is a very expensive undertaking, but just how expensive might surprise you.

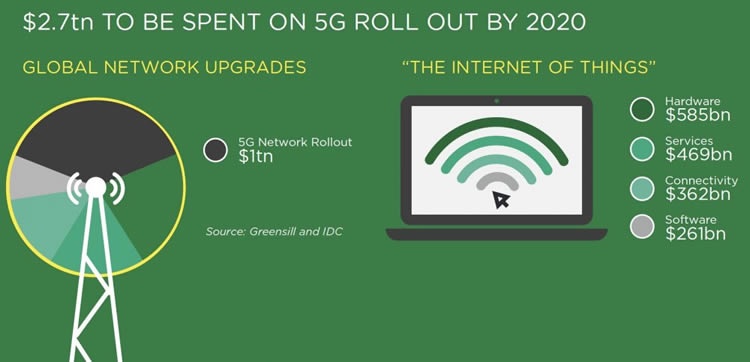

Globally according to analysis from Greensill (a provider of working capital finance) the cost could exceed $2.7 trillion by the end of 2020. But only around $1 trillion of that is expected to go into direct 5G infrastructure investment, with the bulk being required to realise the potential of the internet of things – which is set to be one of the main features of 5G that makes it differ from 4G.

It’s an enormous sum of money and even on the network infrastructure side it’s higher than was once expected, with mobile networks paying far more for 5G spectrum at auctions than was predicted.

As an example, the report notes that a spectrum auction in Italy in autumn 2018 raised €6.55 billion, rather than the €2.5 billion many commentators had expected. And there are concerns that similarly high spending could occur at upcoming spectrum auctions in the UK, which might take place this year.

Can't count on customers

That wouldn’t be such a problem if networks could count on growing subscriber numbers to pay the sum off, but that’s seemingly not something that they can rely on any more, as subscriber numbers have reportedly reached a plateau, one which the promises of 5G may not overcome.

This in turn makes investors wary of pumping money into networks, which could leave the likes of EE, Three, O2 and Vodafone in a tricky situation, where they’re unable to comfortably fund the needed 5G infrastructure.

So what’s the solution? According to Greensill strategic partnerships are one part of it.

Tony Wonfor, Greensill managing director and telecom industry veteran, explains: “The natural direction for this to go is shared infrastructure and shared networks which is very difficult to achieve given entrenched competitor and investor positions.

“Operators want to provide their services but don’t want to make a huge infrastructure investment spend only for it to be repeated by other players in their market, because that results in over-building network.”

But partnerships needn’t just be between mobile networks. They could also for example be between a network, an equipment manufacturer, a data firm and a car company (the latter of which becomes relevant because 5G could help with connected and self-driving vehicles).

These sorts of partnerships could allow for the creation of new supply chain models, which according to Greensill could ease cashflow pressure and risk by leading to shared costs, and may even lead to lower prices for consumers.

We could also see networks embrace new working capital models, such as those developed by Greensill itself. In the handset business, Greensill has set up off-balance sheet purchase facilities, which can ease debt levels in businesses that are often highly leveraged, by creating bonds sold to investors secured on the handset receivables. It believes similar thinking could be applied to mobile networks.

Certainly, something needs to be done, as not only are costs set to be high, they – along with potential returns - are also likely to be spread over 10-12 years according to industry watchers, rather than the 6-8 years that was seen with 4G, so it could take longer for networks to make their money back.

Still, if networks can make the initial investment work, there’s a lot of money to be made, so 5G could have a very bright future.

James has been writing for us for over 10 years. Currently, he is Editorial Manager for our group of companies ( 3G.co.uk, 4G.co.uk and 5G.co.uk) and sub-editor at TechRadar. He specialises in smartphones, mobile networks/ technology, tablets, and wearables.

In the past, James has also written for T3, Digital Camera World, Clarity Media, Smart TV Radar, and others, with work on the web, in print and on TV. He has a film studies degree from the University of Kent, Canterbury, and has over a decade’s worth of professional writing experience.